278/365 I may earn a bonus reward if you use the referral links contained in this article. Thank you for your support!

With the beginning of the new quarter, it’s time to reevaluate what’s in our wallets. While it’s not what Jennifer Garner is looking for, let me walk you through how I decide what credit cards to put at the front of the stack.

Chase Freedom

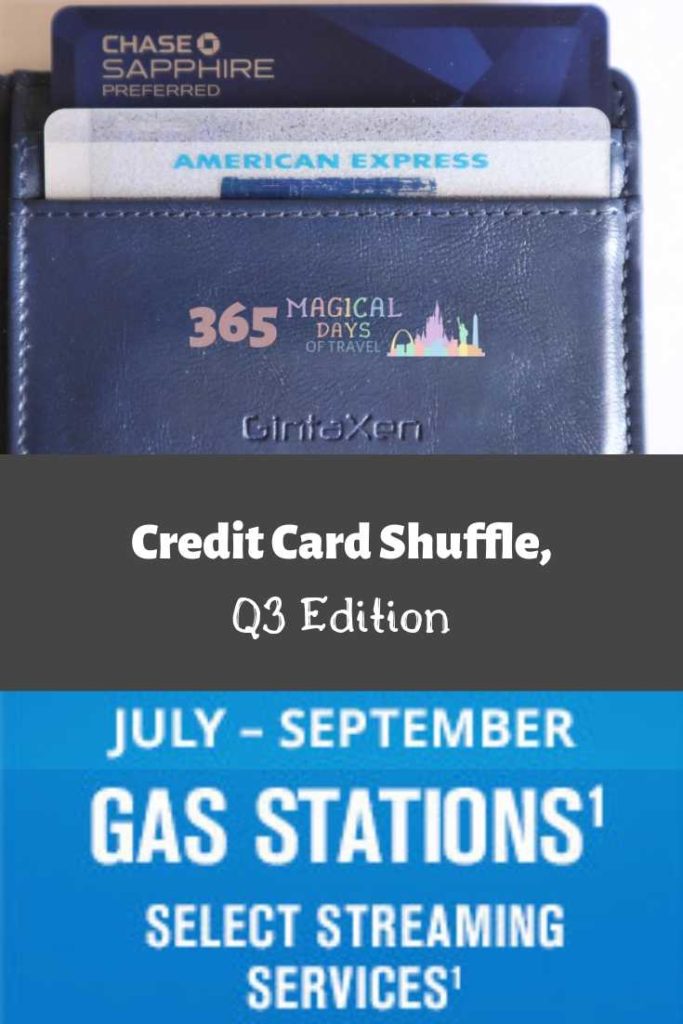

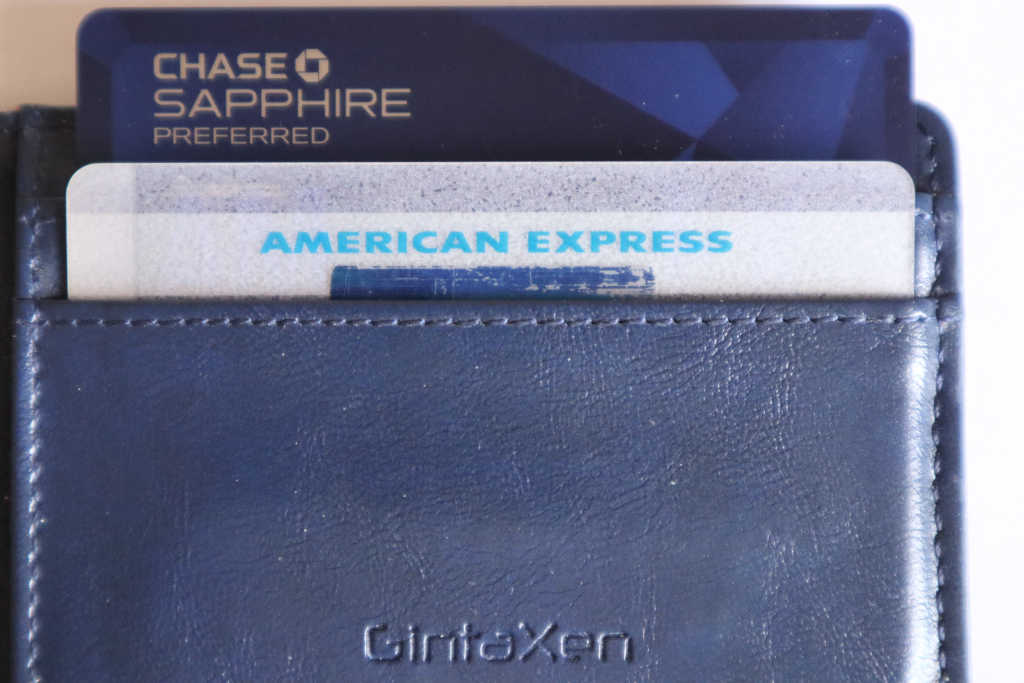

This is the one card that most of the other card decisions rest upon since it changes every quarter and Ultimate Rewards are so very valuable. This quarter (July-September, 2019), the categories are gas stations and streaming services. This presents a very interesting dilemma since the American Express Blue Cash Preferred just added streaming services as a 6% cash back category two months ago. (Read my article on the change here.) Do I really want to change over all of my streaming services’ billing cards for three months? Not really, but 5x is better than 6% any day. I just don’t feel like the time investment is worth the return. I guess I’ll have to rely on gas stations to fill the rest of the $1500 max on each of our Freedom cards this quarter. We have a couple of road trips planned, but we don’t spend that much on fuel each month. This may be one of those quarters when we don’t maximize our 5x Freedom bonus.

Changing It Up for Restaurants

For restaurants, I used to rely on my Chase Sapphire Reserve for 3x points, but I recently realized that I should be pulling out my Citi Prestige for 5x at restaurants. I discovered that I can get great hotel deals on longer trips by using my ThankYou points to book hotels with the 4th night free. While this benefit has changed to only twice per year, it will be a great value when paid with points. I’ll have to start racking up the points from restaurants between now and the next time we have a stay where we can use a 4th night free. I am going to miss all of the Ultimate Rewards points from the Chase Reserve, for sure.

Other Cards

For my other spending, I have different cards that serve different purposes. For office supply, I always use our Chase Ink Business Plus that earns 5x Ultimate Rewards. However, I need to call Chase to downgrade to the Cash version since it will also earn 5x, but without the annual fee. For most all other purchases, I keep a Visa or MasterCard gift card in my wallet that I’ve purchased at a discount from an office supply store for 5x Ultimate Rewards or at a grocery store for 6% cash back on the American Express Blue Cash Preferred. This is the way I maximize my spending and carry my rewards earning over to purchases that wouldn’t normally earn rewards. We finished the spending on Bryan’s World of Hyatt card early, so that’s been put into the sock drawer for now.

Accessing Ultimate Rewards

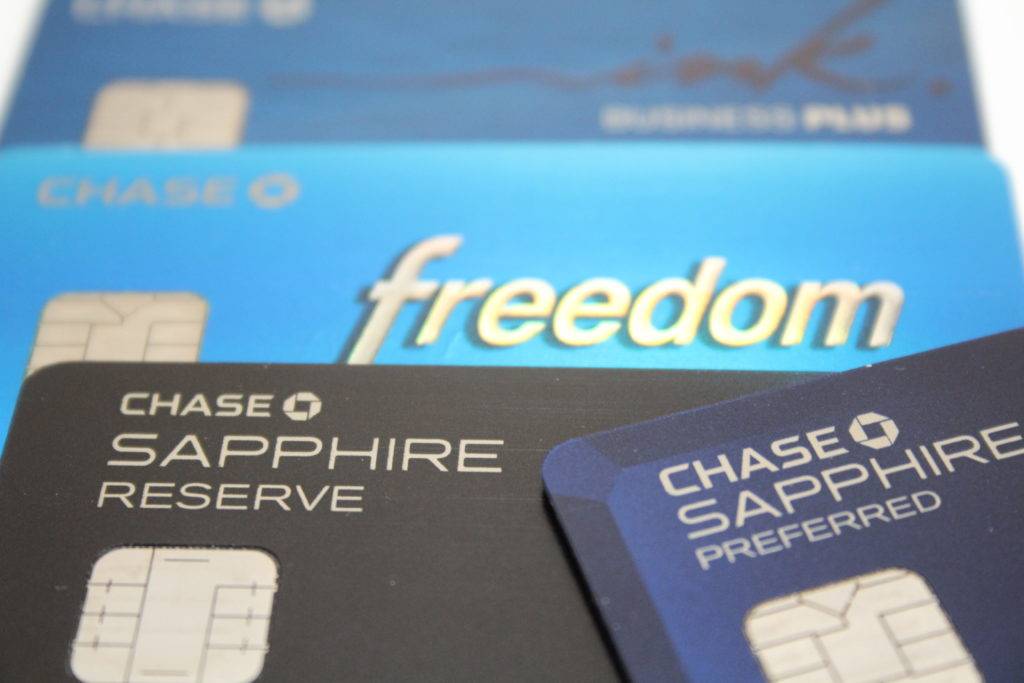

In order to make your Chase Freedom work with Ultimate Rewards, you’ll need a “premium” Chase card to open that portal and allow transfers between points earning accounts. A good starter card is the Chase Sapphire Preferred. This is the premium card that we use on Bryan’s account. It gets 2x on travel and dining, so we don’t put much spending on it. It’s mostly just a placeholder at this point.

Any of the premium (read: annual fee) Ink Business cards from Chase will also allow you to access Ultimate Rewards. A better strategy here, though would be to get one of the premium business cards for the bonus, and then downgrade it to the Cash version for the 5x earning at office supply stores, paired with a Sapphire product to access Ultimate Rewards. (You can read about maximizing Chase Ultimate Rewards in this article.) Whew! That’s complicated!

Simplifying for a Reluctant Spouse

As you can see above, this strategy of maximizing your household spending can become insanely complicated! Some of us may have spouses that are reluctant to have to stop and think (or worse, pull out a cheat sheet) every time they go to checkout. After a couple of years of trying to get my husband to know which cards were which, he bought a new wallet for himself that only holds two credit cards. Message received! Since most of his purchases are at the grocery store, I limit his wallet to a grocery card and an everything else card. Currently, the two cards in his wallet are the American Express Blue Cash Preferred for groceries and Chase Sapphire Preferred for everything else. I would rather he carry the more valuable Chase Sapphire Reserve like I do, but authorized users cost $75 per year, and his spending probably wouldn’t add up to that much in points. The same goes for the $50 annual fee for adding him to my Citi Prestige.

What’s in Your Wallet?

While our quarterly credit card shuffle is literal for my husband’s wallet, it’s mostly a virtual shift in thinking for me. I used to keep a cheat sheet in my purse, but I’ve gotten to know my cards well enough not to have to refer to it as much. Most of my strategy comes from trial and error and simply figuring out which is the best way to maximize our spending.