Day 23/365 2018-2019

So now that you’ve begun to look at your finances, we’re going to look at something very basic to any budget plan: Money In, Money Out. And we’re going to go old school on this one. So get out a notebook or pad of paper and settle in with a cup of your favorite drink, this might take awhile.

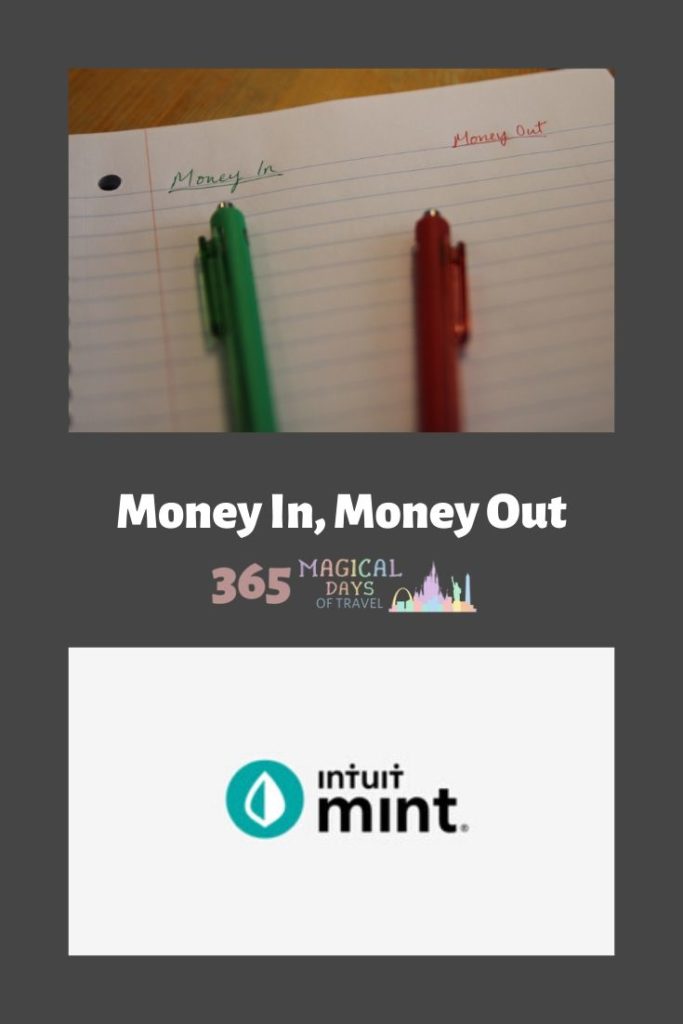

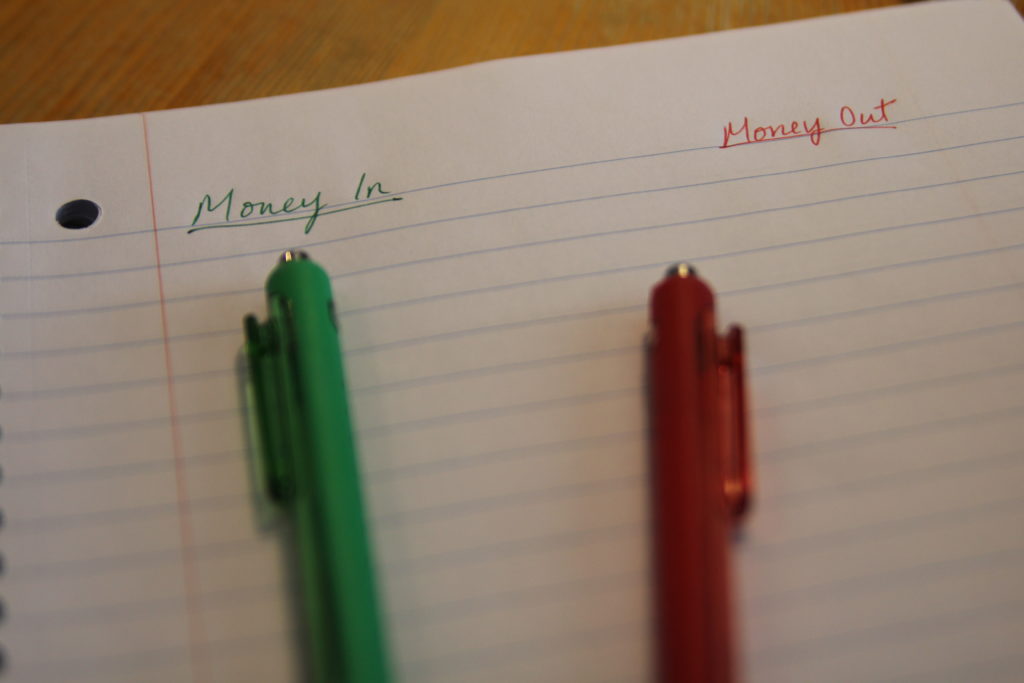

Money In

Now the one side, Money In, probably isn’t going to take very long if you only have one or two sources of income. You may have a second job or receive regular money from some other source. If it’s regular, add it here. If it’s not, leave it off. Bonuses are just that, bonuses. You shouldn’t count of them for your regular budget. Since it’s not easy to compare bi-weekly income to monthly bills, go ahead and do some calculations to see how much income you have on a monthly basis. If you get paid bi-monthly, this will be a snap, but if you get paid bi-weekly, you will have to do some maths. Basically, just take your average paycheck, multiply by 26, and then divide by 12. That should give you a rough estimate of how much you make monthly.

Money Out

On the other side, list all of your expenses. Hopefully, you set up an account with Mint so this will be easier, but if you didn’t, just start with your regular monthly bills: utilities, housing, car payments & insurance, etc. Include anything where you make a regular, monthly payment. Then move on to expenses that aren’t monthly, like annual subscriptions or memberships, car maintenance, school & office supplies, prescriptions, clothes,gifts, haircuts, medical, allowance, home improvement and maintenance, and the list goes on. As you can see, having a tool like Mint will help you gather this data much quicker and put it into a slick pie chart. And I haven’t even mentioned those absolute necessities like groceries and gas which might be harder to get an accurate monthly amount or even estimate!

Drill In

Take some time with this. Do some research. If you have a debit or credit card that you use for expenses, go back through your statements to get a clearer picture. Some of the patterns will surprise you. If you use cash, how do you track your spending? Perhaps you keep a log or a register. Or perhaps you just spend until the cash is gone. Either way, try to see if you can get a rough idea of how you are spending your money over a period of at least a few months.

Now Compare

Once you have your Money In and Money Out columns completed, add them up and compare them. Are you surprised by the result? Not surprised, but wish it were different? This is the point where you look at each column and try to find the places where you can cut back. This process is not easy, but is so rewarding once you have the mechanisms in place to ensure you don’t have to worry about your budget (too much, anyway).