73/365

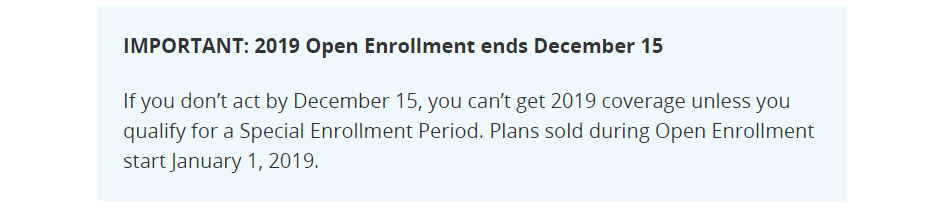

Open Enrollment for healthcare insurance is from now until December 15, which is less than a week away. If you need to sign up for health insurance, or make any changes to your current policy, now is the time to do it. Even if you’re not making any changes, you’ll likely still have to turn in some sort of form or another stating that you don’t want to make any changes. Whew!

FSA Was a Bust

Several years ago, we learned about the Flexible Spending Account (FSA) program. This was a bank account of sorts that we could use to pay for out of pocket healthcare expenses with pre-tax money. It was extremely inflexible, though. You have to estimate your out of pocket expenses for the next year and then if you don’t spend it all by the end of that year, you lose it. I’m not sure who it defaults to, because that was your money you saved to the account in the first place.

It really makes no sense. Every year in December, I was scrambling to spend up the account, throwing boxes of bandaids and ibuprofen and anything else I could find in the pharmacy aisle at Target wondering how in the heck I was going to have enough in my cart for the balance of our FSA. Most of the time, too, Bryan’s HR person would have to decline some of my items since they weren’t allowed. You have to have a doctor’s prescription for over the counter medication like ibuprofen. FSA really only covers copays, deductibles, and prescriptions, plus some very specific medical equipment.

HSA To The Rescue

Then we found out about the Health Savings Account (HSA). This is an actual account that earns interest, even dividends if you hit a certain threshold (your insurance deductible) and decide to invest the portion over and above this threshold. This is pre-tax money that is deducted from your paycheck and deposited into an account that you either access with a debit card or submit receipts for reimbursement.

Earn Rewards with Healthcare Purchases

That is where the beauty of the HSA really shines for us. Since you can pay your expenses out of pocket and get reimbursed straight back into your checking account, it becomes an easy way to earn rewards on your credit card. Sure, it’s an extra step, and you have to remember to keep your receipts and upload them to the portal, but it is very beneficial. Plus, this is all tax-free money!

Now, an HSA is only available to those who choose a high-deductible health insurance plan. For Bryan’s company, we have three choices: PPO with a $1000 deductible, PPO with a $2000 deductible, and an HSA plan with a $4000 deductible. It was a gamble for us to switch to the HSA plan the first year, but now, we have over $10,000 socked away in our HSA that would more than cover our deductible if needed. Also, the premium for our plan is much lower than other plans, so we just did the math and took what we had been spending on premiums and put it toward our HSA contributions. This didn’t change our take-home pay, and that money is available to us for future health care expenses. Plus, we’re earning interest and/or dividends on our money. All while being tax-free!

Protect Yourself from Medical Debt

Now is the time to really sit down and evaluate your health insurance needs. Catastrophic healthcare costs can really cripple your budget and, for an alarming number of people, cause bankruptcy. The statistics are hard to find because people don’t have to state reasons for filing bankruptcies but this is an interesting article that outlines some of the facts about medical debt. My husband unfortunately has seen medical debt affect his extended family and wants to be sure that our family is protected in the event of a catastrophic illness. Even though $10,000 is a good start, we’d like to have more in our account that we can count on if we need it.

Evaluate Your Situation

Our healthcare costs have been relatively low due to the ACA stipulation that companies could keep their current plans. Apparently, that policy has expired, because now our plan has quintupled in cost for 2019, even with switching to a lower cost insurance company. We’ll have to sit down and evaluate our HSA contributions since Bryan’s take home pay will be reduced with the increase in premiums. We’d like to keep up our rate of contribution, but that may not be realistic with our current budget. This is where each family has to take a look at their own budget and make the choice that is best for them. But seriously consider switching your family to an HSA to allow some protection against medical debt, and to reap the rewards from your credit cards.